Oil and CAD: in pain together

Europe keeps trying to get through Brexit and deal with Italy. Equity and oil prices tumbled, and investors’ mood remained sour. This is not a good time for riskier assets. This is not a good time for the Canadian dollar.

The Canadian currency fell to the lowest levels since June versus its US counterpart. The CAD has a strong link with the global risk sentiment. As a result, to reverse in the bullish direction versus the USD it needs recovery in oil and stocks. And it doesn’t seem like this will happen.

The Dow Jones and S&P 500 indices have both erased their year-to-date gains. Oil is one of Canada’s major exports and therefore an important element of its economy. West Texas Intermediate (WTI) oil prices returned to the October 2017 minimums. US sanctions on Iran crude exports have so far failed to actually limit supply and support the price. The reason is that the largest buyers of Iran’s oil (China, India, Japan, and South Korea) were allowed to continue purchases, and so the market doesn’t perceive American sanctions as real. The United States, Russia, and Saudi Arabia, in turn, keep pumping large volumes of oil.

OPEC nations will meet Vienna on December 6 to consider reducing crude-oil production by around 1 to 1.4 million barrels per day. US president Donald Trump wants a lower oil price as he said that OPEC shouldn‘t cut production. He also supported Saudi Arabia following the alleged murder of journalist Jamal Khashoggi by Saudi agents. As a result, Saudi Arabia may refrain from big oil production cuts in order not to disappoint Trump. Overproduction may be.

Will the 200-week MA (yellow line) be able to support the oil price? Or will it just plummet to the next Fibo level (51.50)? Resistance is at 57.40/60.00.

Other factors like the slowdown in China’s economic growth and the trade war between the Asian nation and the United States also kill traders’ appetite for risk (and demand for oil). There may be some political announcements and comments at the G20 summit next week.

Is there any source of light for the CAD from the domestic front? There is, but it hardly seems enough in the current conditions.

The government’s Fall Economic Statement turned out to be business-friendly, but the Bank of Canada Senior Deputy Governor Carolyn Wilkins made some comments that were considered dovish. Alberta NDP MP Rachel Notley warned that the price gap between Canadian and international oil poses a “real and present danger to the Canadian economy.” Canada will release CPI and retail sales figures later today. Retail sales growth may have gathered pace improving a relatively disappointing quarter. The October inflation reading is expected to remain subdued.

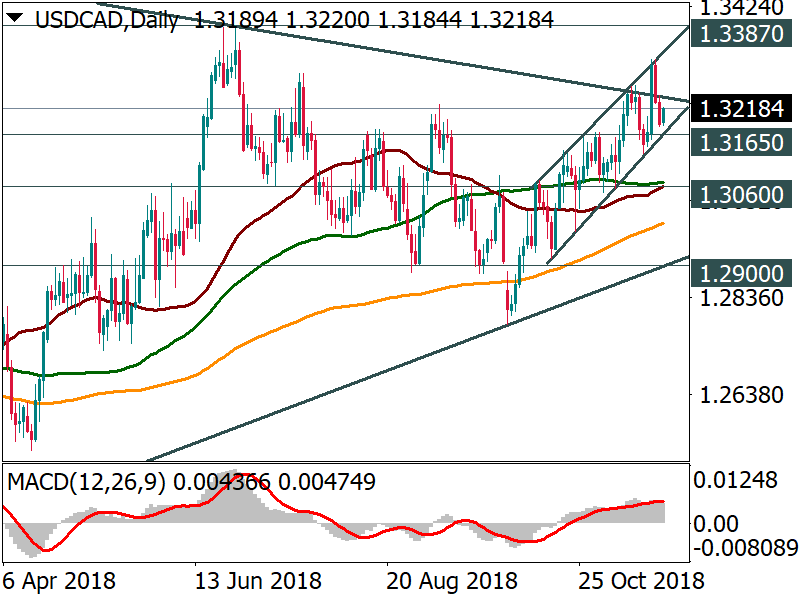

USD/CAD met resistance line connecting April and June highs but still has a chance to rise to 1.3387. Support is at 1.3165 ahead of 1.3060.

To sum it up, oil and the CAD have some technical support nearby and can have a short-term reprieve given the fact that the recent figures from the US disappointed. However, Canada's domestic data are not super bright and the overall grim investor sentiment has a high probability of continuing. As a result, the fundamental analysis suggests that the pressure on oil and the CAD will resume.